The European system of integrated social protection statistics (ESSPROS) provides a coherent comparison between European countries of social benefits to households and their financing, thus making an international comparison of the administrative national data on social protection possible. However, the existing data collection covers gross expenditure on social protection benefits, but there are also cases when the benefits paid to recipients are reduced by direct taxation. This means that a comparison between countries or over time of gross benefit expenditure can be misleading.

This report presents the first estimates of “net social protection benefits” in Estonia for 2005. Net social protection benefits are defined as the value of social protection benefits excluding taxes and social contributions paid by the benefits recipients complemented by the value of “fiscal benefits”.

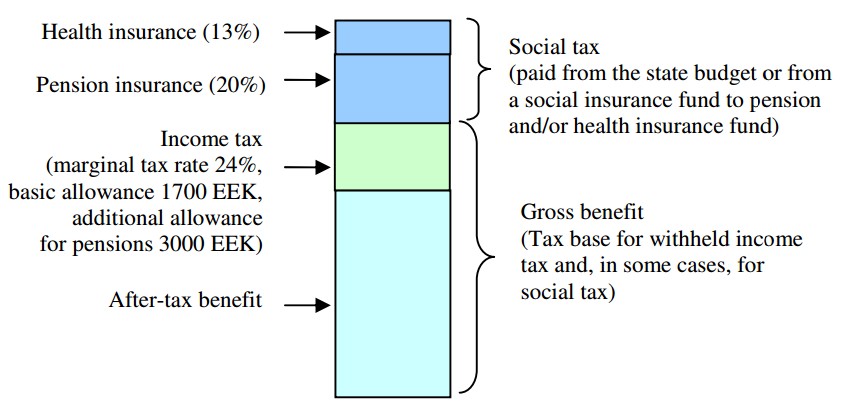

In Estonia there are a few benefits taxed by income tax. They are mainly contribution based benefits. Universal benefits are not taxed. Some benefits are also taxed by social tax, but the tax is always paid from the state budget or by a respective insurance fund and this is not an obligation of benefit recipients. A few benefits that are essentially wage compensation are also reduced by contributions to the funded pension scheme if benefit recipients have joined the scheme.

Schematic composition of taxation of benefits, in 2005

Different approaches to calculate net benefits in Estonia are illustrated in the study:

- aggregate approach – division of withhold taxes and gross benefits as recorded by the institutions paying out the benefits

- individual based microdata approach for pensions – using micro data from the pension register of the Estonian National Social Insurance Board and the tax rules applied to the pensions we simulate tax contributions for each individual and calculated simulated withhold tax rates and average tax rate

- household based microdata approach – using tax-benefit micro-simulation model ALAN we calculate after-declaration tax contributions.

The results show that using the aggregate approach will most likely overestimate the real tax burden, especially for those benefits where basic allowance is not taken into account. However, compared to other approaches, this would be the best solutions currently. Using the microsimulation model will allow to take into account various additional aspects of tax system, but the current model suffers from small sample size, which does not allow very precise results. The most promising approach would be to use final income tax liabilities from the registry data, but this approach would require combining different data and currently Estonian institutions do not have the access to this combined data source.